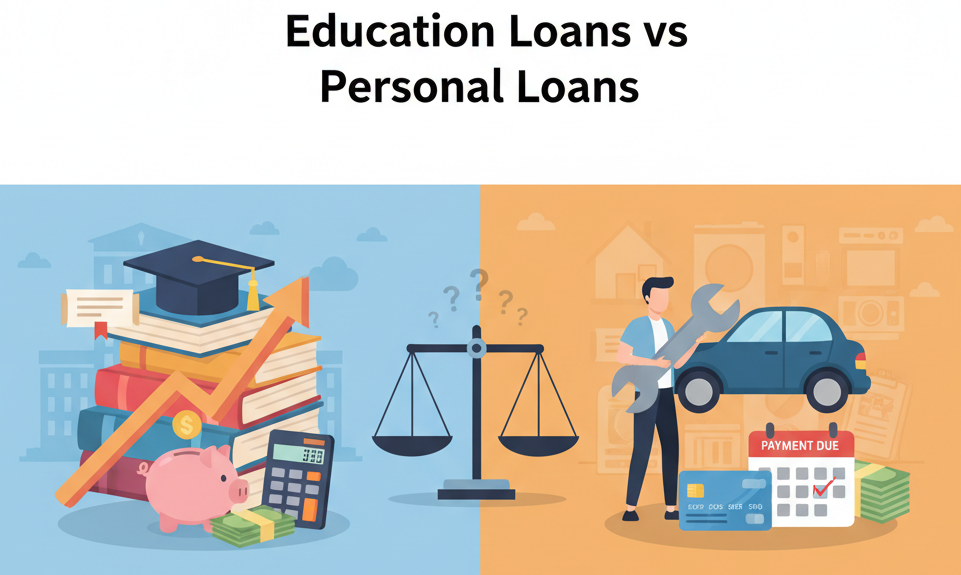

Which is better? Education Loans vs Personal Loans. The federal student loans are usually more protective and have lower rates compared to personal loans for education expenses. But on the other hand, personal loans are faster and more flexible, and they also do not require enrollment.

This comparison guide includes the apparent advantages and disadvantages, the comparative cost examples, the criteria of qualification, and the situation examples when one option is more effective.

What Are Education Loans?

Federal Student Loans

Direct Subsidized Loans: This category of loans is offered to financially needy undergraduates; the government pays the interest as long as you are still in school, and you attend school at least half-time.

Direct Unsubsidized Loans: These loans can be provided to undergraduate and graduate students regardless of their financial need; the interest on this loan is charged at the time it is disbursed.

PLUS Loans: Available to graduate students and parents of dependent undergraduates; does not depend on income but on a credit check.

Repayment Flexibility: Income-Driven Repayment (IDR) plans vary with income, hardship deferral, by forbearal of repayment.

Forgiveness Programs: Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and other programs can cancel any remaining balances.

Important Note: Federal loans have the best protections for U.S. borrowers.

Private Student Loans

Banks, credit unions, and online lenders providing credit-based underwriting education financing are considered to be the private lenders. The interest rates are also tied to credit ratings and income, with rates ranging from 4% to 14% APR for qualified borrowers with good credit.

Nearly all the private loans need to be cosigned by students with limited credit backgrounds or income records. Protections of the borrower are reduced as opposed to federal loans- there are no IDR plans, a weaker deferment, and no forgiveness programs.

Typical Uses for Education Loans

Education loans cover tuition and compulsory charges, lodging and food, textbooks, supplies, and occasionally transportation or rent costs.

There are annual and aggregate borrowing limits of federal loans based on dependency status and grade level.

What Are Personal Loans?

Unsecured Personal Loans

Personal loans offer lump sum financing with fixed monthly payments that are fixed and have terms that last between 2-7 years.

The interest rates are determined in the fixed term of the loan with the APRs of 6-36 percent, depending on the creditworthiness and the lending bank.

No security is needed, though the loan will be approved based on credit rating, income, debt-to-income ratio and employment status.

Secured Personal Loans

Certain lenders provide secured personal loans that are secured by savings accounts, vehicles, and so on.

Secured options are often offered at an APR at a lower rate between 3-10 percentage points compared to unsecured loans, but could face the risk of losing assets in the case of default of payments.

Common Uses for Personal Loans

Education may be financed by personal loans, but more often, it is used to pay off debts, to renovate a home, or to address other emergency needs.

The lenders do not limit the use of funds, so borrowers may use the proceeds to purchase any legal entity, such as living expenses.

The underwriting concentrates on credit scores (usually 580 and above), verifiable income, as well as debt-to-income ratios of less than 40-45%.

Pros of Education Loans

Federal Student Loan Advantages

Minimal Credit Requirements: Subsidized and unsubsidized loans do not come with credit checks; PLUS loans are lax in credit requirements.

Lower Interest Rates: Federal rates are usually lower than personal loan rates, particularly in cases where the borrower has a poor credit history.

Flexible Repayment Options: The Income-Driven Repayment plans limit the payments to 10-20 percent of discretionary incomes with forgiveness of 20-25 years.

Deferment and Forbearance: Interim payments in the periods of unemployment, financial difficulties, or further education.

Forgiveness Programs: PSLF cancels unpaid balances following 120 qualifying payments by public service employees.

No Prepayment Penalties: You can pay off loans early, without extra interest or a charge.

Private Student Loan Advantages

Competitive Rates for Strong Credit: Competent credit consumers with cosigners can get a rate as low as or lower than federal ones.

Higher Borrowing Limits: The Federal loans and aid may not be sufficient to meet all the costs of attendance, which are provided by private loans.

Cosigner Release Options: There are lenders that will release cosigners upon consecutive, on-time payments, usually 24-36 months.

Tax Benefits

Student loan interest deduction gives an option of the deduction of up to $2,500 of interest payment that is qualified each year to the qualified taxpayers.

Cons of Education Loans

Federal Student Loan Limitations

Borrowing Limits: Dependent undergraduates have an annual range of between $5500-$12500, which does not necessarily fully cover.

Disbursement Timeline: Schools are not receiving and disbursing funds based on immediate needs, but based on the school’s academic calendars.

Long-Term Debt Risk: Long-term repayment under IDR plans may result in a high amount of interest paid over the period of 20-25 years.

Origination Fees: Federal loans have an origination fee of 1.057% (Direct) up to 4.228% (PLUS) based on disbursement.

Private Student Loan Limitations

Cosigner Often Required: Students usually require creditworthy cosigners, which imposes a burden on the family and risks.

Limited Protections: No federal IDR plans, no stricter deferment policies, and no forgiveness program eligibility.

Variable Rate Risk: There are also private loans whereby the rates are variable and may go through the roof over time.

Warning: Do not borrow more than what you think you will earn after graduation or what you can comfortably afford to pay back.

Pros of Personal Loans

Personal Loan Advantages

Fast Funding: Online lenders can quickly give loans and fund within 1-3 business days, which is far faster than federal lending.

Flexible Usage: There is no limit on how it can be used; it can be spent on tuition, living expenses, training programs, or to pay off debt.

Fixed Payments: There is the predictability of fixed monthly payments and the certainty of payoff dates, which make budgeting easy.

No Enrollment Required: Does not have to demonstrate school enrollment or continue to make a certain academic progress.

Debt Consolidation Benefit: Can consolidate the high-interest credit card debt at a lower rate in a personal loan.

Cons of Personal Loans

Personal Loan Disadvantages

Higher Interest Rates: APRs are usually higher than the federal student loan rates, particularly when a borrower has fair or poor credit.

No Federal Protections: No access to IDR plans, forgiveness plans or federal deferment/forbearance options.

Credit-Dependent Approval: Approval and competitive rates will require good credit scores (usually 640+) and verifiable income.

Shorter Repayment Terms: 3-5 year terms equate to a greater monthly payment than a 10-year typical student loan repayment.

Origination Fees: There are lenders who impose 1-8% origination fees, which make borrowing expenses more expensive.

Prepayment Penalties: It is not common, however, in some cases, lenders will impose a fee on the early payoff; do not accept this without verification.

How to Decide: 5 Practical Rules

Rule 1: Take federal student loans first if you can get them. First- protections, flexible repayment and the option of forgiveness are better than the cost.

Rule 2: You should only use private student loans when all the federal loans, scholarships, and grants have been exhausted, and you should only do it when you have good credit or a cosigner.

Rule 3: Choose personal loans to use for non-tuition such as living costs, training, or to pay off high-interest debt.

Rule 4: Compare the aggregate costs during the period of your anticipated repayment with calculators that consider all the fees and interest rates.

Rule 5: For Emergency funding outside of academic schedules, please use personal loans with credit unions as an option instead of predatory high-cost lenders.

Real Cost Scenarios

Scenario Comparison: $5,000 Loan

Federal Unsubsidized Loan:

- Interest Rate: 5.50%

- Standard 10-Year Term

- Monthly Payment: $54

- Total Repayment: $6,496

- Total Interest: $1,496

Income-Driven Repayment Effect:

- Payment based on income (potentially lower)

- Extended to 20-25 years

- Total interest: $2,500-$3,500+

- Remaining balance potentially forgiven

Private Student Loan:

- Interest Rate: 8.50%

- 10-Year Term

- Monthly Payment: $62

- Total Repayment: $7,440

- Total Interest: $2,440

Personal Loan:

- Interest Rate: 15%

- 5-Year Term

- Monthly Payment: $119

- Total Repayment: $7,140

- Total Interest: $2,140

Cost Analysis Summary

| Loan Type | Monthly Payment | Total Repayment | Total Interest | Term |

| Federal (Standard) | $54 | $6,496 | $1,496 | 10 years |

| Federal (IDR) | Varies by income | $7,500-$8,500 | $2,500-$3,500 | 20-25 years |

| Private Student | $62 | $7,440 | $2,440 | 10 years |

| Personal Loan | $119 | $7,140 | $2,140 | 5 years |

Education Loans vs Personal Loans: Qualification Checklist

Federal Student Loans Requirements

- Complete FAFSA (Free Application for Federal Student Aid) annually

- U.S. citizen or eligible non-citizen status

- Valid Social Security Number

- Enrolled at least half-time in an eligible degree or certificate program

- Maintain satisfactory academic progress

- No default on previous federal student loans

- Male students: registered with Selective Service (if applicable)

Private Student Loans Requirements

- Credit score typically 650+ (or creditworthy cosigner)

- Verifiable income or cosigner income

- Enrollment verification at an eligible institution

- U.S. citizenship or permanent residency (most lenders)

- Debt-to-income ratio consideration

- Age of majority in your state (18-21, depending on location)

Personal Loans Requirements

- Credit score minimum 580-640, depending on the lender

- Verifiable steady income (employment, self-employment, retirement)

- Debt-to-income ratio below 40-45%

- Valid identification and Social Security Number

- Active checking account for disbursement

- Employment history or stable income documentation

Tax, Forgiveness & Policy Notes

Federal Loan Forgiveness Programs

Public Service Loan Forgiveness (PSLF): Service can be used to forgive the outstanding loan amount after making 120 consecutive payments of qualifying monthly payments under full-time employment at a government or nonprofit.

Teacher Loan Forgiveness: The teachers who teach for five years in low-income schools will have up to $17,500 in loan forgiveness.

Income-Driven Repayment Forgiveness: The remaining balances are forgiven following 20-25 years of qualifying payments under IDR plans.

Eligibility Requirements: Strict criteria apply; check the eligibility in StudentAid.gov before using forgiveness programs.

Tax Deductibility

Student loan interest deduction provides a deduction of up to $2500 of student loan interest payments annually.

There are income eligibility requirements: there is a phase-out starting at $75,000 (single) or $155,000 (married filing jointly) in 2024.

The interest on personal loans is not deductible as the loan is not applied to qualified education expenses, and there are certain criteria to be met by the IRS.

When Consolidation/Refinance Makes Sense

Refinancing Student Loans

Potential Benefits: Reduction in interest rates that borrowers with enhanced credit quality have, ease in making payments when loan consolidation is done in one way.

Critical Drawback: Turning the federal loans into private loans wipes out all the federal protections, such as IDR, forbearance, and forgiveness.

Best Candidates: Stable high-income, excellent credit, do not require federal protections and forgiveness programs.

Debt Consolidation with Personal Loans

Good Strategy When: Credit card debt (with an interest rate of 18-25%) needs to be consolidated into personal loans that are charged at lower rates (8-25%).

Poor Strategy When: Consolidating low-rate student loans into higher-rate personal loans to make them easier to pay.

Decision Checklist:

- Compare the weighted average current rate to the new personal loan rate.

- Divide the total interest over the respective period of repayment.

- Take into account the loss of any federal protections.

- Assess penalty on prepayments and origination costs.

Red Flags & Predatory Lending Signs

Warning Signs to Avoid

Upfront Fees: According to the legitimate lenders, they never charge money before approving or dispensing loans.

Guaranteed Approval: There is no legitimate lender that guarantees approval without viewing credit and income information.

Pressure Tactics: Pushy sales, hard-sell or limited-time offers are a sign of predatory practices.

Vague Terms: Unclear interest rates, concealed fees, or unwilling to give out written loan agreements in prior form.

Unverifiable Servicing: No physical address, lack of licensing or absent data to confirm the credentials of lenders.

Specific Red Flags

Very Short Terms: Personal loans of 6- 12 months for large sums generate unmanageable payment spikes.

Processing Fees: Exorbitant initial processing or application fees in excess of normal origination charges.

No Credit Bureau Reporting: Lenders that do not report the payments deny you a chance to have a credit history.

Frequently Asked Questions

Which is better for tuition: education loans vs personal loans?

Federal student loans are more advantageous in terms of tuition because they offer reduced rates, flexible repayment, and protection for the borrower. Personal loans should be used as a last resort to federal loans.

Can I refinance federal student loans with a personal loan?

Yes, but that goes away with all federal protections such as income-based repayment, forbearance and forgiveness programs. You should just think about whether you are earning a steady income and you also have good credit.

Do personal loans affect eligibility for student loan forgiveness?

Paying federal loans with personal loans will make the borrower ineligible for forgiveness, as only federal loans are eligible in programmes such as PSLF.

Are private student loans reported to credit bureaus?

Yes, student loans that are made privately are reported to credit bureaus to have a positive or negative impact on your credit score, which in my case, is positive due to on-time payments and negative due to late payments.

Can I use a personal loan to pay for college and still complete FAFSA?

Personal loans do not change the eligibility of FAFSA. Further borrowing is, however, likely to have an impact on the following years’ Expected Family Contribution figures.

What if I have bad credit—which option is better?

The subsidized/unsubsidized loans do not require any credit checks for federal student loans. Personal loans require fair to good credit (580+) as a requirement.

How fast can I get funds from personal loans vs student loans?

Funding of personal loans takes 1-3 days of the business. Federal student loans are paid at school times, usually 7-14 days in the beginning of the semester.

Are there tax benefits to either loan type?

Both federal and private student loans are deductible to a maximum of up to 2500 in interest per year. The interest on personal loans is usually not deductible.

Should I take maximum federal loans even if I don’t need them now?

Only borrow what you need. The loan capacity not utilized will not be taken up in the semesters to come without interest income.

Where can I compare different loan options quickly?

Utilize comparison sites that present preapproved lending options with different lenders and you can quickly review the rates and terms based on your credit history.

Conclusion

So what should you choose? Education Loans vs Personal Loans. Your initial choice in funding your education should be federal student loans since they provide better protections, offer you to pay easily and in some cases, you can have them forgiven. When federal loans, grants, and scholarships cannot fund the entire expenses, specifically with good credit or cosigners, private student loans can be used as an addition.

Personal loans are most effective when it comes to non-tuition, fast funding outside of the academic school year, or when it comes to consolidation of high-interest debt that is not related to education. You can think about employing detailed comparison tools like theloans.pro to compare all your options and identify the most cost-effective one to deal with this particular case.