In recent years, securing a personal mortgage or small-business advance often felt more like gathering evidence for a court case than discovering a flexible financial option. Mountains of forms, handwritten corrections, repeated interviews; the entire ordeal dragged on through busy work, sorting, photocopying, and lunches forgotten in briefing folders. Most borrowers trudged through the lull because they needed credit, yet they openly wished technology would please pick up the tedious bulk. Enter 2025. The same relief that turns cellphone cameras into instant photo labs is now available in lending. With artificial intelligence quietly threading dozens of internal and external datasets, eight questions spoken into an app can yield a firm approval in forty-eight seconds. Behind that zippy alert lies fully digital underwriting, mechanical risk-tuning, and an operations playbook designed to sidestep lost faxes or stamped signatures altogether. In this post we walk through the nuts and bolts driving the clock forward, the code, sensors, and safeguards lending a twenty-first-century edge, and what the very quick answer means for your wallet tomorrow.

What is automated loan approval?

At its cleanest, automated loan approval means the vote on credit – yes, no, maybe tomorrow, comes from software, not from a single analyst stretching between phone calls and calendar gaps. By tapping real-time feeds of credit scores, income verifications, recurring transfers, and even expenses flagged in open-banking records, a trained algorithm can draw a conclusion in seconds.

Because those countless numbers move through program pipelines instead of human eyes tracing line notes, the approach trims calendar days, curbs careless bias, and lets lenders scale at a pace manual reviews never could. Today most midsize online players have embedded some version of the automation stack, and regional bank chiefs admit their paused pilots only look slow compared to the sprint now underway.

Why the Fast Loan Process Matters in 2025

In today’s on-demand economy almost any question can be answered within seconds. That expectation spills over into personal finance too, and borrowers now want loan approval delivered with the same speed. As a result, the speed of the lending process has shifted from a luxury feature to a critical determinant of borrower satisfaction. Waiting weeks for a credit decision was already frustrating; during a power outage, a flat tire, or a broken printer the extra hours crack open a different kind of wound. Medical expenses, late invoices, and equipment failures do not operate on the same timeline as mortgage committees. By shrinking that wait to minutes, lenders give applicants the room to move when life pushes.

Snapshot of the Swift Loan Experience

Most customers now expect the entire journey to feel instantaneous:

- Apply online in five minutes;

- Securely upload pay stubs and ID;

- Sign with a finger;

- Watch the balance arrive, sometimes within a few hours.

That rhythm has been made possible by advances in artificial intelligence, cloud computing, and integrated payment rails, all working behind the scenes.

The Role of Digital Underwriting

At the heart of that rapid guitar solo lies digital underwriting, the engine that swaps human eyes for code yet keeps fairness in view. Instead of passing a file from officer to officer, algorithms can scour credit reports, bank feeds, and employment records in milliseconds.

When you press submit, the platform:

- Collects every relevant data strand;

- Weighs them against thousands of historical patterns;

- Issues an approval or denial in seconds.

Because the model relies on transparent variables rather than subjective intuition, it also has the potential to level the playing field across genders, zip codes, and ethnicities. That blend of speed and equity makes digital underwriting the unofficial backbone of the fast loan process heading into 2025, and its unlikely to lose that title soon.

How Artificial Intelligence Is Revolutionizing Lending

AI in lending now stands for more than speed; it also signals smarter risk choices. By analyzing thousands of historical applications, the technology continually refines how lenders assess creditworthiness.

Here are a few everyday advantages lenders gain:

- Predicting borrower defaults with remarkable precision

- Spotting fraudulent activity as it tries to enter the system

- Proposing custom loan sizes and interest rates for each applicant

Those features let banks reach consumers once considered too risky or invisible. Gig workers, freelancers, and others with non-traditional incomes can now be assessed based on their whole financial story. When this insight pairs with completely online underwriting, lenders launch the most advanced automated approval engines yet.

Real-World Examples of the 1-Minute Loan

Several companies already show what fast, fair AI-driven lending looks like:

- Upstart processes personal-loan requests, checks documents, and makes a yes-or-no call in approximately sixty seconds.

- SoFi expedites approval for student and private loans, lifting outcomes while keeping underwriting guidelines secure.

- Kabbage monitors real-time revenue streams and offers small-business owners instant funding snapped up on a smartphone.

These names champion a principle: speed and accuracy are no longer in conflict.

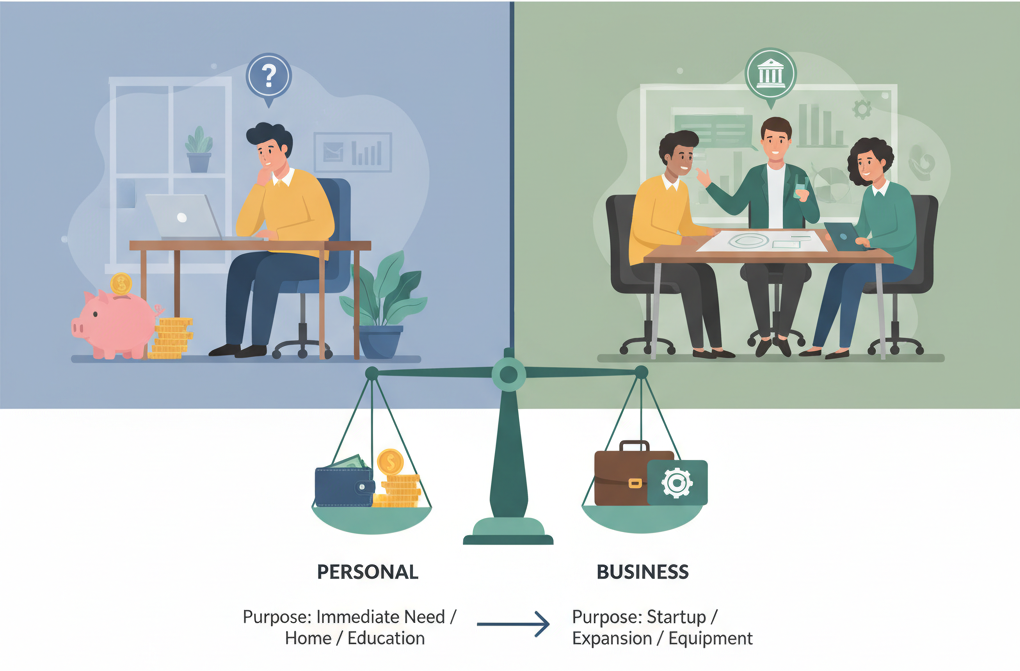

Benefits for Borrowers and Lenders

Automation cuts the costs of origination and servicing, sparing borrowers unwanted fees while allowing banks to invest freely in customer growth.

For Borrowers:

- Instant approval decisions

- Much lighter paperwork

- Better rates through digital underwriting

- Around-the-clock account access

For Lenders:

- Lower operating costs

- Fewer processing errors

- Rapid scaling capacity

- Enhanced customer satisfaction

All this comes from automated loan approvals and advancing AI in the industry.

Is It Safe?

Potential borrowers frequently ask whether this technology is secure. The truthful answer is yes, assuming vendors implement best practices. Responsible lenders encrypt data, use secure APIs, and follow strict rules to protect personal information. Indeed, AI often identifies potential fraud signals faster than human analysts. With digital underwriting, every step leaves a trace, adding another layer of transparency.

Even so, it remains wise to examine any lender thoroughly before submitting an application.

The Future of AI in Lending

The future looks bright-and remarkably fast. As more banks adopt artificial intelligence, approvals will accelerate further, and loan products will feel more tailored. Picture receiving mortgage clearance in under five minutes; that scenario is plausible within a few years. Automated underwriting systems will continually improve, expanding affordable credit access worldwide.

Final Thoughts

A one-minute loan no longer belongs in the realm of dreams; it is already underway. By blending AI, automated approvals, and digital underwriting, lenders now deliver a rapid process that fits the pace of modern life.

If you plan to borrow money next year, look for a lender that uses cutting-edge tools. Using speedier technology can trim weeks off your timetable and sometimes put cash in your account before your morning coffee cools.

FAQs

What is automated loan approval?

Automated loan approval means a computer system reviews your files and generates a yes-or-no answer in seconds, without human touch.

How does AI help in lending?

AI analyzes past patterns-learning software hunts for risk signs, flags possible fraud, and suggests loan terms that fit each customer.

What’s the benefit of digital underwriting?

Digital underwriting replaces slow paperwork with data scans, so decisions reach borrowers faster and error rates drop.

Can I really get a loan in one minute?

Absolutely. With today’s tech, a few lenders promise full approval and even cash delivery in under sixty seconds.