Embedded finance lending is a way to borrow money instantly, in the store, in apps, or when paying bills no extra visits to the bank needed.

It occurs by giving a seamless borrowing experience within the platforms you are already using, including e-commerce checkouts, fintech applications and digital wallets.

The guide includes the kind of embedded loans, their operation and advantages, risks and considerations when selecting safe borrowing.

What Is Embedded Finance Lending?

The loans are taken out by borrowers with the help of the platforms they use regularly, such as e-commerce platforms, ride-hailing applications, or online wallets.

You do not have to go to banks and complete individual loans, but seek credit where you need it in a familiar application.

Common Examples:

- Buy Now, Pay Later options are appearing at online checkout

- In-app payday advances through fintech platforms

- Installment loans embedded in marketplace purchases

- Microloans on the digital wallets

Key Difference from Traditional Loans: There is no additional loan application process; all approval decisions are immediate, and the loan is repaid through existing accounts.

Embedded lending eliminates any friction inherent in the borrowing process by incorporating financial services into non-financial platforms and user experiences.

How Embedded Loans Work for Consumers

Users apply within an app or platform; loan approvals are made on the spot or in several minutes; funds are deposited into accounts or finalized purchases.

Typical Application Process

Select Loan Amount: Choose a loan amount at checkout or in the app, depending on what you are buying or the money you require.

Soft Credit Check: Typically evaluates your eligibility without affecting your credit score in any meaningful way.

Instant Approval: Automated underwriting with transaction history, income information and credit profile.

Funds Disbursement: Completes your purchase or cash deposit into your linked account.

Repayment Schedule: Begins automatically with a series of payment plans or planned payments.

Soft vs. Hard Credit Checks

Soft Credit Checks: Check credit without scoring, prequalification and most embedded lending decisions.

Hard Credit Checks: Can cause a temporary drop in credit score by 5-10 points, needed when borrowing a bigger loan or when it is the first loan.

Soft checks are also essential for user experience and minimizing the credit score effects of most embedded lending platforms.

Types of Embedded Finance Lending Products

The various embedded loans are available to consumers based on the platform, intended use, and the sum of money required to borrow.

Buy Now, Pay Later (BNPL)

Short-term installment loans appear at online and in-store checkouts and they divide the purchases into manageable payments.

Typical Repayment Terms: 2-6 installments over 6-12 weeks, automatically made by way of linked accounts.

Interest Rates: Often 0% APR if paid on time; interest charged when payment is late.

Popular Providers: Affirm, Klarna, Afterpay, and PayPal provide BNPL in thousands of merchant checkouts.

Best For: Online shopping, shopping in bulk, which puts a strain on monthly budgets and credit building, which is done by reporting payments.

App-Based Personal Loans & Microloans

Fintech apps offer short-term and small loans, which offer emergency cash to people in need.

Typical Amounts: $50-$5,000 based on platform, income check, and borrowing record.

Approval Speed: Instant to one day funding based on automated underwriting, based on banking data and employment information.

Common Providers: Earnin, Dave, Brigit and MoneyLion provide small personal loans and salary advances on mobile apps.

Best For: Emergency expenses, bridging gaps between paychecks, and avoiding overdraft fees.

Credit Lines in Apps

The revolving credit found in the fintech apps or e-wallets serves similar functions as credit cards, but is much easier to access.

Flexible Repayment: Borrow and repay over and over again within sanctioned credit limits and interest is only paid on to balance.

Approval Factors: Approval is done based on the past spending, the activity of the account, income trends and the behavioral information of the platform.

Interest Rates: The average rates are 15-30% APR, with some sites having 0% offers.

Best For: Ongoing financial flexibility, dealing with variable costs, and escaping the conventional credit card charges.

Merchant & Marketplace Financing

The loans that are installed in online marketplaces and retail platforms allow purchasing more and with a longer repayment term.

Loan Amounts: $500-25,000 based on the size of purchase, creditworthiness, and the relationships with merchants.

Interest Rates: Will commonly include 0% APR (6-24 months) or competitive fixed rates to loyal customers.

Platform Examples: Amazon, Best Buy, Wayfair and large retailers have point-of-sale financing provided by embedded lenders.

Best For: Major purchases, home improvements, furniture, electronics, and building credit through responsible installment payments.

Benefits of Embedded Finance Lending for Consumers

Embedded lending is gaining popularity due to the increased speed, convenience, and the ability to pay in various ways and not visiting a physical bank.

Speed and Convenience

Instant Decisions: Automated underwriting is able to offer approval decisions within seconds, compared to the days that conventional lenders were taking.

No Separate Applications: No need to leave the shopping experience or navigate between different applications.

24/7 Availability: Borrow anytime through mobile apps without the need to wait until the banks are open.

Seamless User Experience

Integrated Interface: Borrowing occurs in familiar applications and platforms that users already know and are familiar with.

One-Click Checkout: With pre-approved credit lines, customers are able to shop instantly without the need to re-enter information.

Automatic Repayment: Linked payment methods repay automatically without manual repayment and forgotten due dates.

Transparency and Credit Building

Upfront Disclosure: View APR, fees, and total repayment plans before loan terms are accepted.

No Hidden Costs: Any hidden costs are evident in the legitimate platforms with no surprises at the repayment of the costs.

Credit Reporting: A good number of the embedded lenders will report payment to credit bureaus and this will assist the users to build credit history.

Payment Flexibility: There are websites where financial difficulties allow altering the payment schedule without heavy fines.

Risks and Things to Watch Out For

Embedded loans are convenient but carry a higher interest rate, contain hidden charges, or may lead to over-borrowing.

Common Pitfalls

Late Fees and Penalties: It is a regular practice to charge some big dollars, like 25-50, whenever you miss payments.

Easy Over-Borrowing: With unhindered access, it is easy to borrow a number of loans to the extent of overstretching repayment.

Higher Interest Rates: There are embedded lenders who impose APRs on microloans that are above the normal personal loan rates.

Variable Regulatory Oversight: Not every embedded lending platform will be subject to identical consumer protection principles. This is important to know for safe online lending.

What to Verify Before Borrowing

APR Disclosure: Confirm lenders are explicit in stating the annual percentage rates and all fees and interest.

Credit Check Type: Learn about the use of soft or hard credit inquiries on applications that affect the scores.

Repayment Terms: Read carefully regarding the exact amount of payment, the date of payment and the consequences of late or missed payment.

Lender Licensing: Check that platforms are registered and licensed in your state and have the necessary consumer protection.

Data Security: Platforms should be encrypted and should adhere to standard finance data security protocols.

How to Choose the Right Embedded Loan

Compare rates, terms of repayment, credibility of the lenders and the security of the platforms before accepting embedded loan offers.

Selection Criteria

Interest Rates and Fees: Calculate the total cost of borrowing money, such as the originating fee, late fee, and interest fee.

Repayment Flexibility: Evaluate platform capabilities to early pay off, modify payment schedule or temporarily forbear.

Lender Reputation: Research reviews on Trustpilot, Better Business Bureau, and Consumer Financial Protection Bureau complaint databases.

Licensing and Compliance: Check whether the lender is licensed in accordance with the websites of state regulators and whether the laws protecting consumers are observed.

Platform Security: Look at HTTPS encryption, privacy policy, and safe authentication of personal information.

Credit Reporting: Find out whether lenders are going to report payments to credit bureaus, in case it is important to build credit history.

Red Flags to Avoid

Guaranteed Approval Claims: No legitimate lender will give a guarantee without looking at financial information and creditworthiness.

Upfront Fee Requests: Avoid platforms that ask you to pay upfront in order to receive the loan before it is disbursed, unless it is explicitly stated.

Vague Terms: Steer clear of lenders who do not specify APR, the conditions of repayment of the debt, or the overall cost of borrowing.

Pressure Tactics: The legitimate platforms provide time to review and draw comparisons without high-pressure selling techniques.

Tips for Responsible Borrowing

Only Borrow What You Need: Do not be tempted to take as much credit as you can get when you do not need to use all of it.

Borrow Strategically

Calculate Total Cost: This should take into account the interest and charges during the entire repayment period and not the monthly payment amounts.

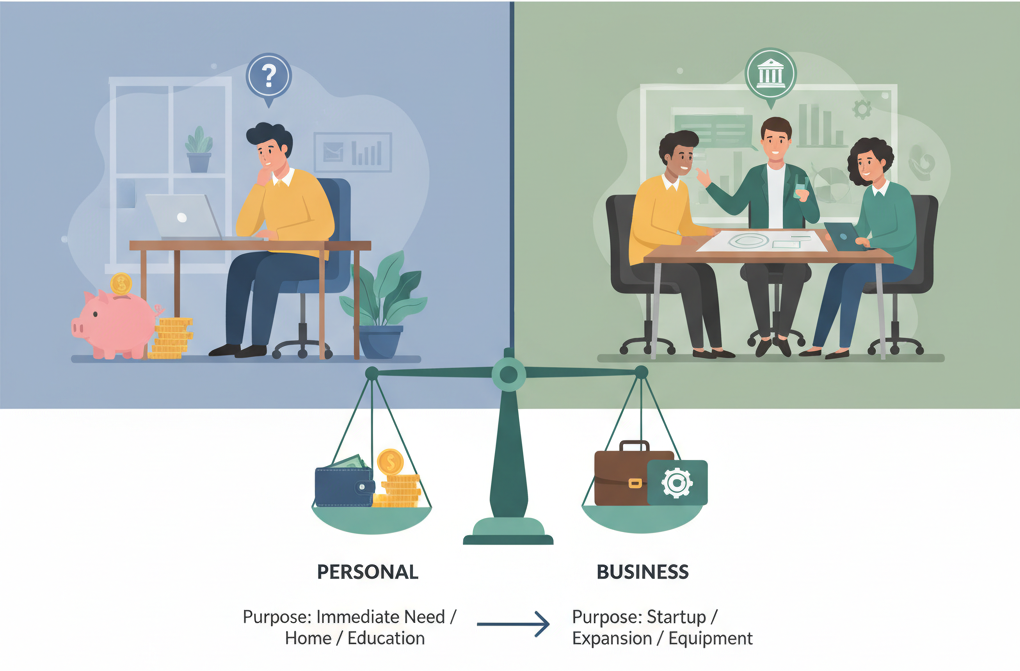

Compare Alternatives: Determine which, between traditional personal loans and credit cards, is more appropriate for your case.

Manage Repayment Effectively

Track Due Dates: Calendar notifications or application reminders can help users prevent payment and late fee charges.

Enable Automatic Payments: Connect credible sources of payment and make sure that there is enough money by the set dates.

Monitor Multiple Loans: When working with multiple embedded lending platforms, over-commitment can be avoided by keeping track of all obligations.

Use Technology Wisely

Payment Reminders: Turn on push notifications and email alerts on lending applications when a payment becomes due.

Budget Integration: Integrate lending applications with budgetary tools to monitor the influence of borrowing on general financial well-being.

Regular Reviews: To evaluate all ongoing loans, interest rates and balances between platforms frequently.

Know When to Choose Traditional Options

Lower Interest Rates: The conventional personal loans of the banks or credit unions tend to be better charged on larger sums.

Longer Terms: Bank loans offer long repayment terms that limit monthly payments on high costs.

Better Protections: Existing financial institutions can provide more detailed consumer protections and dispute resolution mechanisms.

Frequently Asked Questions

What is an embedded loan?

An embedded loan is a credit that is integrated into non-financial applications such as shopping apps, a marketplace, or other fintech services, without distinct applications.

How quickly can I get funds?

Most embedded loans are instant approval, where the funds are received within a few minutes to 24 hours, as compared to traditional bank loans, where funds take a long time before they are disbursed.

Does it affect my credit score?

Several embedded lenders conduct soft credit checks that do not affect scores. Hard questions can be asked concerning greater sums and will reduce the score by 5-10 points.

Can I pay off early?

Most embedded loans enable early repayment without chargebacks, though you must ensure terms are checked before borrowing. Interest can be saved by paying in advance.

Are BNPL loans interest-free?

Many BNPL options will have a 0% APR provided they are paid during the promotion period. Late payments can initiate fees and interest.

Is it safe to borrow inside an app?

Lending via known and certified platforms under safe encryption is usually secure. Reviews and lender credentials must always be checked before applying.

What happens if I miss a repayment?

Late payments typically incur fees ($25-50), might result in interest payments, and might be reported to credit agencies, which might ruin credit scores.

How do fees work?

Commissions are dependent on the platform but generally encompass the late payment charges, origination charges (0 to 5% of the loan) and possible maintenance fees (monthly).

Are embedded loans legal in the U.S.?

Yes, embedded lending is legal, but is subject to various laws across states. The lenders are supposed to adhere to the laws of state licensing and federal laws of consumer protection.

Where can I compare embedded lending options?

Comparison sites such as theloans.pro are used to compare various lending options side by side, displaying rates, terms and comments left by users to make an informed choice.

Conclusion

Embedded finance lending transforms consumer borrowing by enabling the use of credit on daily platforms, making a loan available when one requires it. Embedded lending is very appealing in terms of cash flow management and purchases due to the ease of instant approval and easy repayment.

Always compare rates, ensure the credibility of the lender and clear terms before accepting an embedded loan offer by any platform. For comprehensive comparisons of lending options, including embedded and traditional loans, explore theloans.pro that aggregates offers and helps identify solutions matching your financial needs.