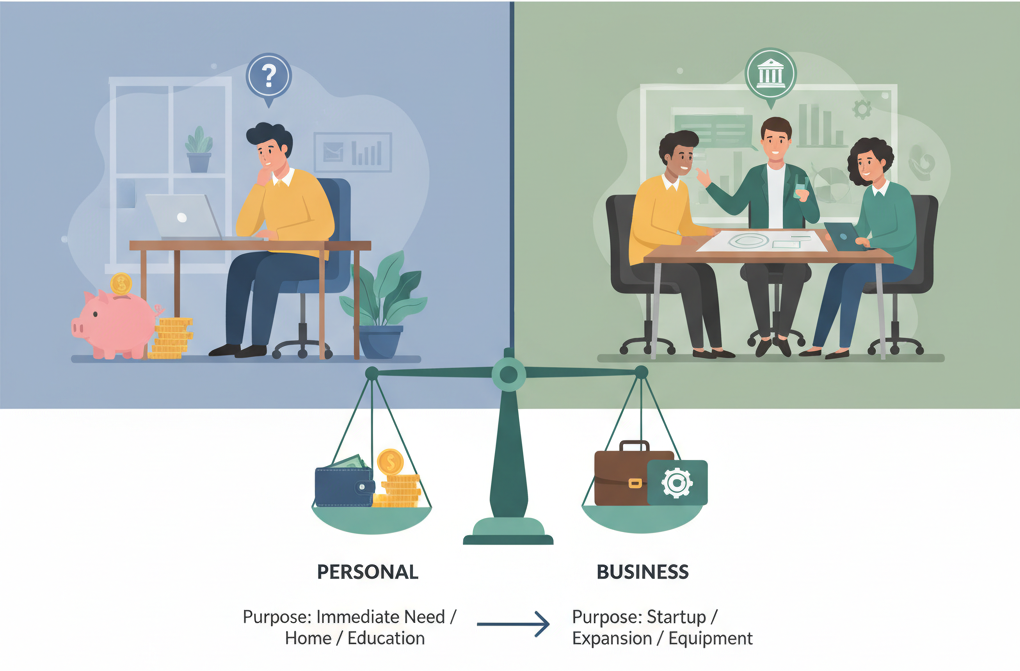

How to choose between personal and business loans? For lower dollar amounts and faster approval, use a personal loan. For larger dollar amounts, better repayment terms, and to keep your business’s finances separate, use a business loan.

This guide will cover the key differences between personal and business loans, help you compare the costs of each, explain the eligibility requirements for both, introduce you to a five-step decision process, and outline common pitfalls to avoid.

What is a Personal Loan vs a Business Loan?

A personal loan is an unsecured type of credit that is based on your individual creditworthiness and an assessment of how well you can pay it back. A business loan uses your business’s creditworthiness, revenues, and assets to determine whether you qualify for the funds you’re requesting.

Personal Loans

Personal loans allow individuals to borrow a specific amount of money at a fixed interest rate and repay it over a predetermined period of time. The lender evaluates the applicant based on their credit score, income, and debt-to-income ratio.

The majority of personal loans are unsecured, which means they do not require the applicant to pledge collateral such as a house, car, or other asset. However, some personal loan products may be secured by collateral such as a savings account or a vehicle.

The lending decision is solely based on the applicant’s personal credit history, their level of employment stability, and their ability to make payments from personal income sources.

Business Loans

Business loans, on the other hand, look at the financial health of the business and the creditworthiness of the business before making a lending decision. Lenders typically review a business’s financial records, including its tax returns, profit and loss statements, cash flow projections, and outstanding business debt obligations, before approving a loan.

Many business loans also require the owner to personally guarantee the loan, thereby exposing the owner to liability for the loan if the business defaults. This creates a “hybrid” liability for the owner, who may face liability for the loan from either the business or the lender depending on the circumstances.

Key Differences

| Feature | Personal Loan | Business Loan |

| Collateral | Usually unsecured | Often requires business assets |

| Typical Amounts | $5,000-$50,000 | $10,000-$500,000+ |

| Terms | 2-7 years | 5-25 years |

| Purpose | Any personal use | Business purposes only |

| Tax Treatment | Not deductible | Interest often deductible |

| Credit Basis | Personal FICO | Business credit + revenue |

When a Personal Loan Makes Sense

You should consider choosing a personal loan for smaller dollar amounts, single-use purchases, rapid access to funds, and when your personal credit rating is solid and you are willing to take on the associated risk.

Ideal Use Cases

Small Equipment Purchases: If you are purchasing a computer, tool, or piece of equipment less than $10,000 and feel that the paperwork associated with obtaining a business loan outweighs the benefits of a business loan.

Freelance Project Funding: When you need funding to cover upfront costs of a contract but the payment for services is delayed until after completion, especially for freelancers and solo entrepreneurs.

Consolidated Business Expenses: When you have multiple small business debts and your revenue is unpredictable or varies seasonally, paying off these debts with a personal loan can be beneficial.

Startup Phase Financing: Businesses that are still in the startup phase and lack a long enough operating history and/or credit profile to qualify for a personal loan.

Advantages of Personal Loans

Easy Application Process: Requires identification, income verification, and credit check—nothing about the business.

Faster Funding: Online lenders can approve and fund in 1-3 business days, rather than weeks for business loans.

Lower Fees for Good Credit: Excellent personal credit will allow one to get competitive rates without business credit building.

No Business Requirements: No need to have established business revenue, time in operation, or a separate business entity.

Disadvantages of Personal Loans

Personal Guarantee Risk: You are fully liable with business success or failure, risking your personal assets.

Smaller Loan Amounts: Typically, loan amounts are capped at $50,000 or less, which isn’t enough for major business expansions or equipment.

Mixed Finances: This is where separation between personal and business finances becomes blurred, complicating bookkeeping and taxes.

Limited Tax Benefits: Interest on personal loans isn’t usually tax-deductible, even if the money is used for business.

Personal Credit Impact: Delinquency or defaults directly affect the personal credit score, impacting future borrowing capacity.

When a Business Loan is Better

Business loans work best for larger funding needs, preserving personal credit, building business credit, and separating liabilities.

Ideal Use Cases

Business Expansion: Setting up new facilities, entry into new markets, or scaling up businesses entailing large capital investment.

Funding payroll expenses during growth phases before revenues related to the new employees show up.

Large Equipment Purchases: Purchases of machinery, vehicles, or technology infrastructure costing greater than $25,000.

Property Purchase: This involves buying commercial property, warehouses, or offices to operate the business.

Long-Term Working Capital: covering continued operational expenses due to seasonal slackness or an extended payment cycle.

Advantages of Business Loans

Builds Business Credit: Establishes a credit profile separate from personal credit, hence providing any future business financing opportunities.

Large Loan Sizes: The availability of six-figure or seven-figure funding for major business investments and expansion.

Tax Deductibility: Interest payments generally constitute business expenditure and, hence, deduct the specified taxable income.

Separation of Personal Credit: This keeps business borrowings separate from personal credit reports and scores.

Business-Friendly Terms: Longer repayment periods, seasonal adjustments of payments, and terms that fit with business cash flow.

Disadvantages of Business Loans

Stricter Eligibility Requirements: Typically requires 1-2 years of established revenue history and good financial statements.

Longer Approval Processing: Underwriting a business loan takes several weeks to months, with voluminous documentation and verification involved.

Collateral Requirements: Business assets, inventories, accounts receivable, or personal guarantees may be required as collateral.

Higher Interest Rates: Newer businesses or those with inconsistent revenue receive higher rates than established companies.

Complex Documentation: Requires business tax returns, financial statements, business plans, and ownership documentation.

Direct Comparison: Personal vs Business Loans

Compare purpose, eligibility, amount, term, cost, tax implications, and liability considerations side by side.

| Feature | Personal Loan | Business Loan |

| Primary Purpose | Small expenses under $50k | Growth, assets, expansion over $50k |

| Credit Basis | Personal FICO score | Business credit + personal guarantee |

| Approval Speed | 1-3 days (fast) | 2-8 weeks (moderate to slow) |

| Documentation | ID, income proof | Business financials, tax returns |

| Tax Deductibility | Generally not deductible | Interest usually deductible |

| Liability | Fully personal | Business entity + possible guarantee |

| Personal Credit Impact | Direct and immediate | Indirect or less significant |

| Typical APR Range | 6-36% | 4-30% (varies by business strength) |

| Best For | Solopreneurs, small needs | Established businesses, large needs |

When ranges overlap-$20,000 to $50,000-consider making careful comparisons between offers for each type of loan.

Cost Comparison & Financial Impact

True cost includes interest, fees, repayment term, and tax treatment; compare APR, total repayment, and deductibility effects.

Example Scenario: $50,000 Loan Over 5 Years

Personal Loan Option:

- Interest Rate: 12% APR

- Monthly Payment: $1,112

- Total Repayment: $66,720

- Total Interest: $16,720

- Tax Benefit: $0 (not deductible)

- Net Cost: $66,720

SBA Business Loan Option:

- Interest Rate: 10% APR

- Monthly Payment: $1,062

- Total Repayment: $63,720

- Total Interest: $13,720

- Tax Benefit: ~$4,100 (30% tax bracket)

- Net Cost After Tax: ~$59,620

Business Line of Credit:

- Interest Rate: 15% APR (variable)

- Monthly Payment: Varies (interest-only option)

- Total Interest: $18,750 (if drawn fully for 5 years)

- Tax Benefit: ~$5,625 (30% tax bracket)

- Net Cost After Tax: ~$63,125

Cost Analysis Summary

| Loan Type | Total Interest | Tax Savings | Net Cost | Monthly Payment |

| Personal Loan | $16,720 | $0 | $66,720 | $1,112 |

| SBA Business Loan | $13,720 | $4,100 | $59,620 | $1,062 |

| Business LOC | $18,750 | $5,625 | $63,125 | Varies |

Decision Factors

Amount Threshold: Personal loans tend to work under $25,000, but business loans are cost-efficient over $50,000.

Term Considerations: Longer terms lower monthly payments but increase total interest; match terms to asset life or project timeline.

Tax Benefit Impact: Business loan interest deductibility can save 20-37% of interest costs depending on the tax bracket.

Decision Framework: 5-Step Checklist

Ask five questions before choosing: What’s the purpose? How much do I need? What can I qualify for? What’s the cost? What risk am I taking?

Step 1: Define Need and Purpose

Identify Specific Use: Clearly articulate if the funding supports a personal need or legitimate business operation and growth.

Justify Business Classification: Ensure that expenses qualify as ordinary and necessary business costs for tax deductibility purposes.

Timeline Review: Consider urgency-personal loans get funded sooner, though business loans might make more long-term sense.

Step 2: Determine Amount and Term

Exact Need Calculation: Calculate the actual funds that are required, keeping in mind a buffer for contingencies.

Match Term to Purpose: Short-term needs of less than 2 years suit personal loans, while long-term investments call for longer business loan terms.

Monthly Payment Capacity: Ensure that payments fit comfortably in the personal or business cash flow without straining it.

Step 3: Assess Eligibility

Personal Loan Eligibility:

- Credit score 620+ (580+ for some lenders)

- Steady income documentation

- Debt-to-income ratio under 45%

- Basic employment verification

Business Loan Eligibility:

- 1-2 years business operation history

- Annual revenue minimums ($50,000-$100,000+)

- Business credit score (DUNS, Experian Business)

- Complete financial statements and tax returns

Step 4: Compare Total Costs

APR Calculation: The annual percentage rate comparison includes all fees for the true cost comparison.

Account for tax benefits: Subtract the business loan costs by the expected tax deduction value according to your bracket.

Include All Fees: Account for origination fees that range from 1-8%, application fees, and potential prepayment penalties.

Project Total Repayment: Calculate the complete cost over the full term, not just the monthly payment amounts.

Step 5: Evaluate Liability and Structure

Personal Guarantee Assessment: Understand whether you will be held personally liable regardless of business structure.

Asset Risk Analysis: Identify what personal or business assets are at risk in case of a default scenario.

Credit Impact Consideration: Assess the impact of each option on personal credit scores and future borrowing capacity.

Legal Structure Review: Verify borrowing is within your business entity type, whether LLC, S-Corp, or sole proprietorship.

Common Pitfalls & How to Avoid Them

The common mistakes include mingling finances, underestimating costs, disposing with taxes, choosing speed over suitability, and not reading the terms.

Financial Mixing Issues

Problem: Using personal loans for business expenses complicates accounting, taxes, and undermines business entity protection.

Solution: Maintain separate business and personal accounts, along with separate credit products. Document the business purpose of each clearly.

Qualification Miscalculation

Problem: Assuming eligibility to business loans without appropriate revenue history forces reliance on personal loans, with guarantees.

Solution: Check the requirements of a lender before applying; build up your business credit and revenue documentation ahead of time.

Payment Structure Mistakes

Problem: The selection of shorter terms and higher payments creates cash flow strain in slower periods.

Solution: Select terms that match cash flow patterns; choose longer terms, if uncertain, but with the option for prepayment.

Hidden Cost Oversight

Problem: Focusing on interest rates alone while excluding origination fees, prepayment penalties, and maintenance charges.

Solution: Calculate total borrowing cost including all fees; request complete fee schedules before signing.

Tax Implication Neglect

Problem: Missing the opportunity to claim major tax deductions or claiming personal loan interest as a business expense.

Solution: Consult a tax advisor before borrowing; keep appropriate documentation for business use claims.

Repayment Planning Failure

Problem: Not considering realistic repayment scenarios, including possible fluctuations in revenues or changes in personal income.

Solution: Model best-case, expected, and worst-case scenarios; ensure ability to repay in all situations.

Frequently Asked Questions

Can I use a personal loan for business purposes?

Yes, personal loans can be used to finance business needs; however, interest is not tax-deductible, plus you bear full personal liability irrespective of business performance.

Do business loans require personal guarantees?

Most small business loans, especially for newer businesses or those without much in the way of assets or credit history, require personal guarantees.

Which loan type builds business credit?

Only business loans that get reported to business credit bureaus build business credit. Personal loans impact only personal credit, regardless of usage.

Can I get a business loan with bad personal credit?

Difficult, but possible. It’s possible with strong business revenue or collateral, or through alternative lenders. Most business lenders check both business and personal credit.

What’s the minimum revenue needed for a business loan?

This varies by lender but generally ranges between $50,000 and $100,000 annual revenue, though some specialty lenders accept less.

Are business loan interest rates lower than personal loans?

Not always-established businesses having good credit get much better rates, while the riskier or more recently established businesses have higher rates than personal loans.

How long does business loan approval take?

Traditional business loans take anywhere from 2-8 weeks, while online lenders may approve within days. Personal loans get approved in 1-3 business days.

Can I refinance a personal loan into a business loan?

Absolutely, you can refinance personal debt into business loans on better terms when your business has built up enough revenue and credit history.

Where can I compare both personal and business loan options?

Platforms like theloans.pro allow direct comparison of different types of loans, using rates, terms, and overall cost for informed decisions.

What happens if my business fails with a personal loan?

You remain fully liable from personal assets and income for repayment. Similarly, business loans with personal guarantees create similar obligations.

Conclusion

So, how to choose between personal and business loans? Your choices between personal and business loans are based on the amount needed, the maturity of the business, tax considerations, and comfort with liability. Personal loans are ideal for smaller amounts-less than $25,000-faster funding needs, and when qualification for a business loan is difficult.

Business loans are valued over $50,000 for established businesses when tax deductions matter, and to build separate business credit. Never rush the decision—compare the total costs, including the tax effects, assess eligibility honestly, and match loan terms to your specific situation. Consider using comprehensive comparison tools like theloans.pro to evaluate all available options and make informed borrowing decisions aligned with your financial goals.